Personal financial management has never mattered so much as it does today. With inflation, higher prices, liberal credit, and an unpredictable market, some are quickly becoming wealthy, and the rest, burdened with financial stress. Individuals managing finances are becoming financially free while others remain in financial bondage. Personal financial management is vital for achieving financial stability, safety, and freedom.

What is Personal Financial Management?

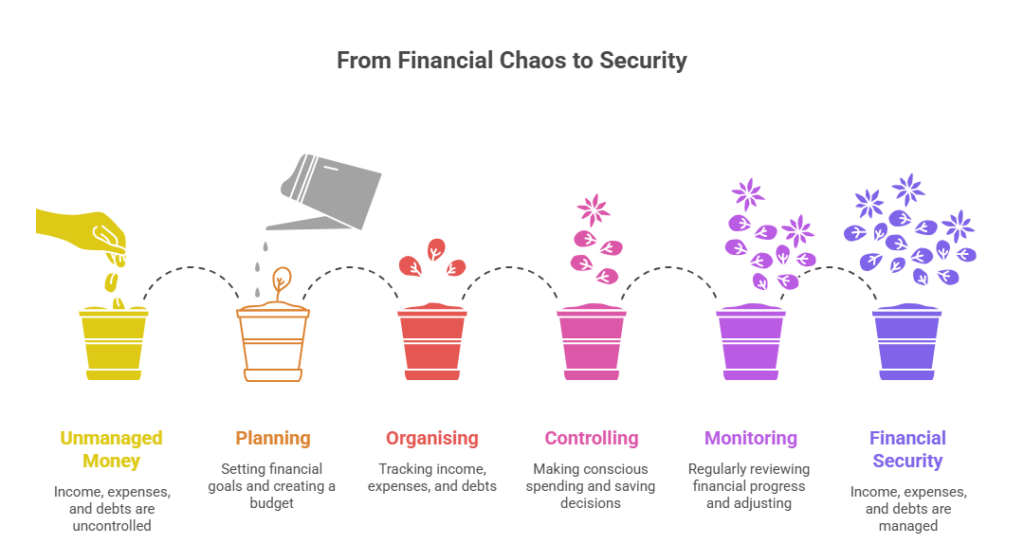

Personal financial management is the planning, organizing, directing, and controlling of one’s finances, savings, expenses, investments, debts, and financial future. It is in the making of financial decisions on one’s earnings, spending, saving, and money growth.

In answering of four questions, one can easily define financial management:

- Where is my money coming from?

- Where is it going?

- How can I make it grow?

- How can I protect it?

The Value of Personal Financial Management in Today’s World

The value of personal finance has rapidly increased over the last few decades. In India, rapidly rising levels of inflation continue to increase prices for most basic necessities, including food, transportation, and shelter. With the advent of credit cards, personal lending is at the center of many young professionals’ spending debt.

Meanwhile, job markets are becoming more volatile with advancements in AI and automation making many jobs redundant. Those equipped with personal financial management skills are better capable of enduring job loss, medical emergencies, or unexpected expenses. Those without such skills, do not manage their finances as effectively and may even live paycheck to paycheck despite earning good salaries.

Major Benefits of Strong Personal Financial Management

The most important benefit of effective personal financial management is financial peace of mind. Financial planning and expense control removes the constant anxiety related to financial stress.

Over time, financial management plays a key role in wealth creation. Good management enables you to save a portion of your income and make important investments throughout your life. Over many years, you will not only have wealth but also be in a position to borrow and obtain credit at more favorable terms.

Another important benefit is that financial management allows you to make better choices in all aspects of your life. With good financial management, you know the position you are in and the choices you have, which allows you to make important life decisions such as purchasing a house, a car, or pursuing post-secondary education.

Key Areas in Personal Financial Management

Effective personal financial management covers several important areas:

- Budgeting is the foundation. Creating a monthly budget helps you understand where your money goes and control unnecessary spending. The popular 50-30-20 rule (50% needs, 30% wants, 20% savings) works well for most people.

- Saving and Investing are equally crucial. Savings give you security, while investing helps your money grow. Starting early with SIPs in mutual funds or fixed deposits can create long-term wealth.

- Debt Management is often ignored but very important. High-interest credit card debt can destroy your financial health. Smart personal financial management means using debt only when necessary and clearing expensive loans first.

- Insurance and Risk Protection protect you and your family from unexpected events like medical emergencies or accidents. Adequate health and life insurance are non-negotiable parts of good personal financial management.

- Retirement Planning should start as early as possible. Contributing regularly to EPF, PPF, or NPS can help you build a comfortable retirement corpus.

Digital Rupee (CBDC) vs. UPI: Is the Era of Physical Cash Finally Ending in India? (2026)

Practical Steps to Improve Your Personal Financial Management

Start by tracking every rupee you spend for at least one month. Use simple apps or Excel sheets to record expenses. Create a realistic budget and review it every month.

Build an emergency fund that can cover 6–9 months of expenses. Keep this money in a liquid savings account. Pay off high-interest debts aggressively. Start investing even with small amounts through SIPs.

Review your financial progress every quarter and adjust your plan. Educate yourself continuously about personal finance through reliable sources.

Common Mistakes People Make in Personal Financial Management

Many people spend more than they earn, have no budget, and ignore emergency funds. Others put all savings in low-return savings accounts or fall for quick-rich schemes. Some delay retirement planning until their 40s, making it much harder to build a decent corpus.

Avoiding these mistakes is one of the most practical applications of understanding the importance of personal financial management.

7 Common Financial Ratios That Can Predict a Startup’s Failure

Final Thoughts

The importance of personal financial management cannot be overstated in today’s uncertain world. It gives you control over your money instead of letting money control you. Start small, stay consistent, and be patient. Financial freedom is not about earning crores — it is about making smart decisions with whatever you earn.

Take charge of your finances today. Your future self will thank you for it.

FAQ – Importance of Personal Financial Management

What is the importance of personal financial management?

It helps you control spending, save money, reduce debt, and build long-term wealth while providing financial security.

How to start personal financial management as a beginner?

Begin by tracking expenses, making a monthly budget, building an emergency fund, and starting small investments through SIPs.

At what age should one start personal financial management?

The earlier, the better. Starting in your early 20s gives you the power of compounding over many years.

Can personal financial management help in reducing stress?

Yes. Knowing you have savings and a clear plan greatly reduces money-related anxiety and improves mental peace.

What is the 50-30-20 rule in personal financial management?

It suggests spending 50% on needs, 30% on wants, and saving/investing 20% of your income.